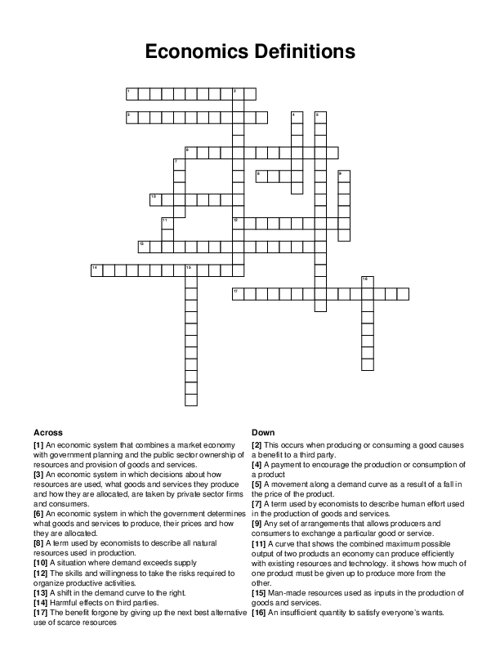

Economics Definitions Crossword Puzzle

Download and print this Economics Definitions crossword puzzle. Use a pencil or pen to complete the puzzle by filling in the blanks. The completed answers are included, so you can easily check your progress.

PDF will include puzzle sheet and the answer key.

Related puzzles:

More Business / Finance Crossword Puzzles

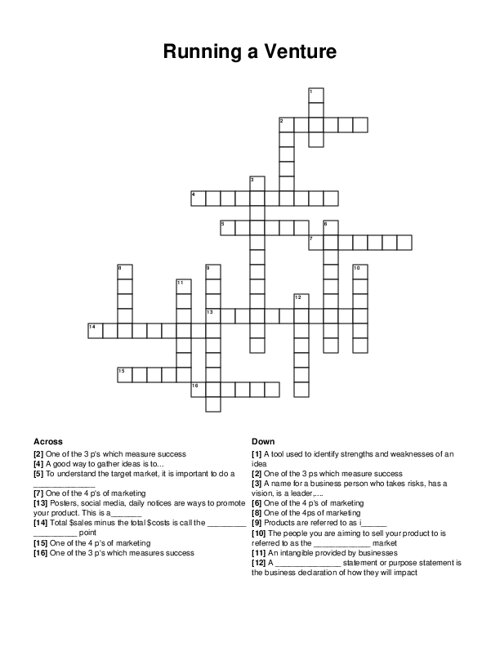

Running a Venture

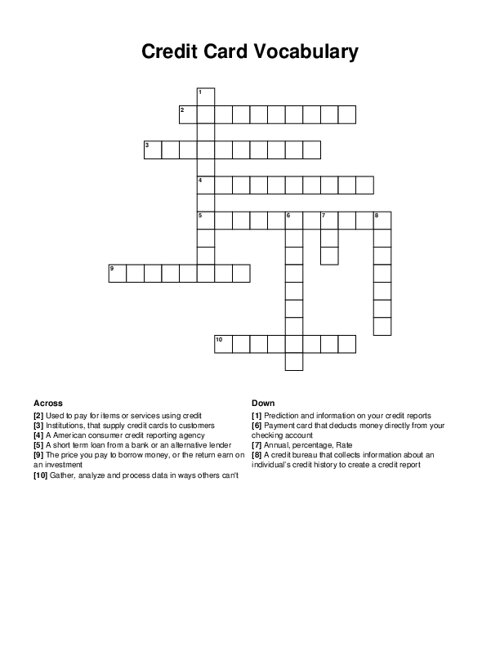

Credit Card Vocabulary

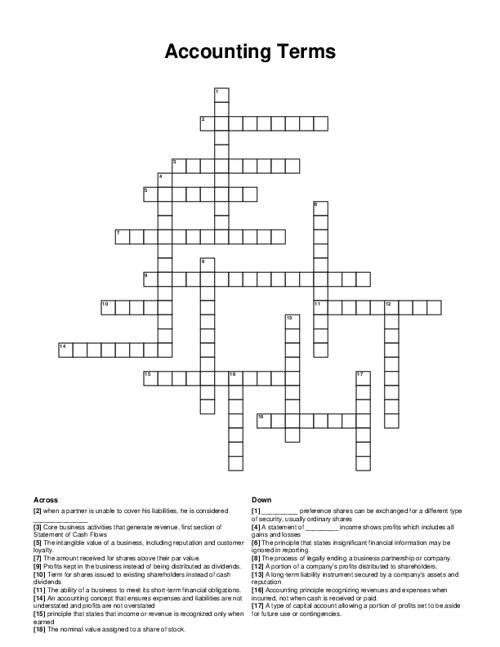

Accounting Terms

Introduction of Economics

Business Key Terms

Browse all Business / Finance Puzzles

QUESTIONS LIST:

- scarcity : an insufficient quantity to satisfy everyone’s wants.

- market system : an economic system in which decisions about how resources are used, what goods and services they produce and how they are allocated, are taken by private sector firms and consumers.

- shortage : a situation where demand exceeds supply

- planned system : an economic system in which the government determines what goods and services to produce, their prices and how they are allocated.

- capital goods : man-made resources used as inputs in the production of goods and services.

- labor : a term used by economists to describe human effort used in the production of goods and services.

- subsidy : a payment to encourage the production or consumption of a product

- opportunity cost : the benefit forgone by giving up the next best alternative use of scarce resources

- market : any set of arrangements that allows producers and consumers to exchange a particular good or service.

- enterprise : the skills and willingness to take the risks required to organize productive activities.

- extension in demand : a movement along a demand curve as a result of a fall in the price of the product.

- mixed system : an economic system that combines a market economy with government planning and the public sector ownership of resources and provision of goods and services.

- land : a term used by economists to describe all natural resources used in production.

- increase in demand : a shift in the demand curve to the right.

- external benefits : this occurs when producing or consuming a good causes a benefit to a third party.

- external costs : harmful effects on third parties.

- ppc : a curve that shows the combined maximum possible output of two products an economy can produce efficiently with existing resources and technology. it shows how much of one product must be given up to produce more from the other.